A collar is a hedging strategy that helps you manage your foreign exchange risk by limiting your exposure to currency fluctuations to within a certain range.

It consists of two option contracts:

- An option you buy that gives you the right to exchange currency at a predetermined rate if the exchange rate becomes too unfavourable for you. This is called the ‘floor’ because it protects you against the worst case scenario.

- An option you sell that gives the purchaser the right to exchange at a predetermined rate if the exchange rate becomes too favourable to you and, so, too unfavourable to them. This is called the ‘cap’.

Imagine you’re a UK business that has imported €40,000 worth of goods from Ireland. You have to pay your supplier in three months’ time.

There are three possible scenarios in the run up to your invoice payment date:

- The GBP/EUR exchange rate goes down from 1.13 to 1.08. This means £1 now only gets you €1.08, rather than €1.13. You need more pounds to get the same amount of Euro, so the goods you’ve imported are more expensive than you expected.

- The GBP/EUR exchange rate moves minimally, going from 1.13 to 1.15.

- The GBP/EUR exchange rate goes up from 1.13 to 1.18. £1 now gets you €1.18. You can get more Euro with fewer pounds, so your goods work out cheaper than you expected.

There are three possible scenarios in the run up to your invoice payment date:

Now imagine you have a collar in which the floor is 1.10 and the cap is 1.15.

In scenario 1, you can limit your loss by exercising your option and getting a better exchange rate than what’s available on the market.

In scenario 2, you can go ahead and exchange at the market rate.

In scenario 3, the party who owns the cap will probably exercise their option to cut their losses. But you haven’t technically made a loss — your exchange rate is only marginally lower than the market rate, and still higher than what it was two months ago.

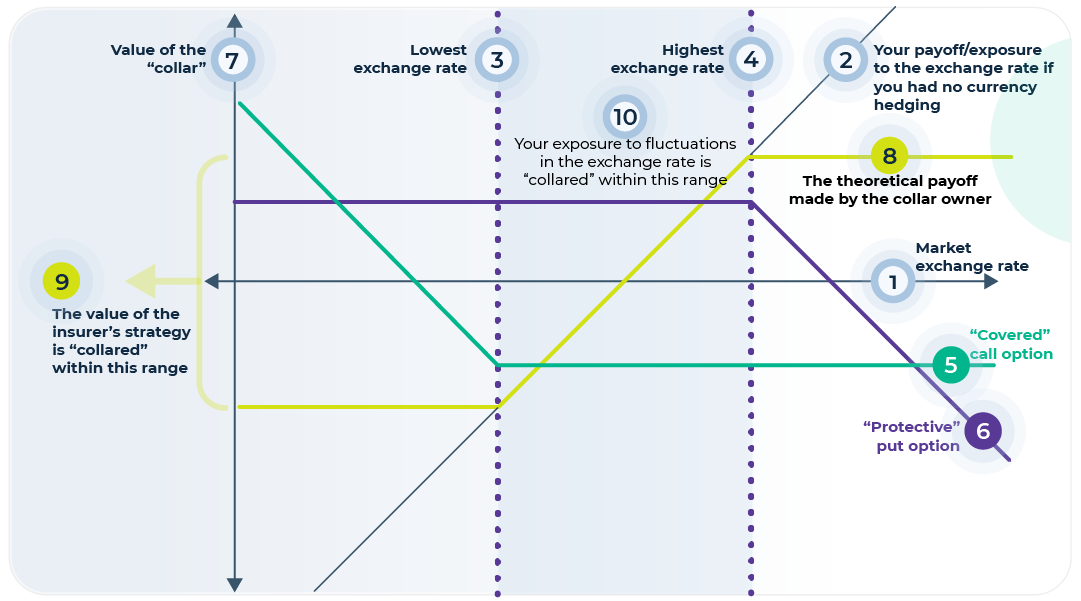

How a foreign exchange collar works?

A hedging strategy that helps limit exposure to currency fluctuations to within a certain range.

TERMINOLOGIES EXPLAINED

1. Market exchange rate (e.g. USD/GBP) against whose fluctuations you want to protect yourself.

2. Your payoff/exposure to the exchange rate if you had no currency hedging

(i.e. no “insurance”); you can see that it is unlimited both upwards and downwards!

3. Lowest exchange rate – You want to insure yourself, because you don’t want to lose too much money if the exchange rate goes against you.

4. Highest exchange rate – You want to insure yourself for, because you don’t care about making a lot of money if the exchange rate goes massively in your favour, as you prefer stability.

5. “Covered” call option – Your insurer sells a call option; this limits their & your exposure to downward exchange rate fluctuations i.e. acts as a “floor”.

6. “Protective” put option – Your insurer buys a put option; this limits their & your exposure to upward exchange rate fluctuation i.e. acts as a “cap”.

7. Value of the “collar” – To its owner (your “insurer”) i.e. the value of the put option bought by them, plus the value of the call option sold by them

8. The theoretical payoff – Made by the collar owner (i.e. your “insurer”). However, most hedging providers also hedge themselves against these payoffs. After all, their business is not gambling on currency movements, but insuring you properly!

9. The value of the insurer’s strategy – (the put option it bought plus the call option it sold) is “collared” within this range.

10. Your exposure to fluctuations in the exchange rate is “collared” within this range

Some Facts

- Collars are a trade-off. The cap means you won’t be able to benefit should the exchange rate become very favourable. But the flipside is that it keeps costs low, because the cap also limits its owner’s risk.

- Collars can be structured so their premiums cancel each other out and there’s no money to pay on either side. For example, you could buy a ‘floor’ for £20 and sell a ‘cap’ also for £20. This is called a zero-cost collar.

- While you might not have to pay a premium upfront, you may have to pay a deposit if the exchange rate moves significantly in your favour before the collar expires.

Want to know more?

- This article discusses how collars are used in emerging markets, where exchange rates are more volatile and other hedging techniques can be too expensive.

- If you don’t mind getting technical, this paper analyses the mathematics of collars and other foreign currency hedging techniques. It also discusses the scenarios where hedging is most important… and when it isn’t such a concern.

ALT21’s perspective:

“If you’re worried about foreign exchange volatility but can’t afford to pay a hefty premium to hedge your risk, a collar might give you the best of both worlds. You can protect yourself at low cost should the exchange rate become unfavourable and still benefit from a favourable exchange rate, albeit only up to a point“.