At the money is a term used in options trading.

Options are contracts that allow you to buy or sell an asset at a pre-agreed price. For example, you could buy an option that gives you the right to exchange £4,000 into US Dollars at an exchange rate of 1.45.

Unlike other types of contract, you go ahead with the exchange only if you want to. As the name suggests, you have an option. But there’s no obligation to buy or sell the asset (or, to stick to our example, to exchange your British Pounds for US Dollars). The idea is that the option acts as “insurance”.

Let’s say your UK business has suppliers in the US, so you regularly exchange British Pounds for US Dollars to pay them.

This creates a risk for your business. If the exchange rate goes down, you’ll need more British Pounds to get the same amount of US Dollars, so your overhead will go up.

An option protects you against this. If the exchange rate available on the open market becomes less favourable, you can use the option to make the exchange at a better rate which you’ve fixed in advance. This gives you certainty.

When an option is at the money, its strike price — the price at which you can buy or sell the asset — is equal to the asset’s market price. So, if the current Pound Sterling to US Dollar exchange rate is 1.45 and you’ve bought the right to exchange pounds for dollars at 1.45, your option is at the money.

Because options at the money are so close to becoming profitable, they typically generate a lot of trading activity.

That said, it’s not usually advisable to exercise options when they’re at the money. This is because the benefit of owning an option is that it acts as ‘insurance’: it provides you with a better alternative when market conditions are unfavourable.

Imagine you bought an option to exchange British Pounds for US Dollars for £20.

If you were to exercise the option when it’s at the money, you’d get the same exchange rate that’s available on the open market, and you’d have paid £20.

In comparison, if you exercised your option when the real exchange rate was 1.36, you’d get an additional $0.09 for every £1 than you’d get on the market — a cool $360 extra in your pocket (minus the £20 you’ve paid).

TERMINOLOGIES EXPLAINED

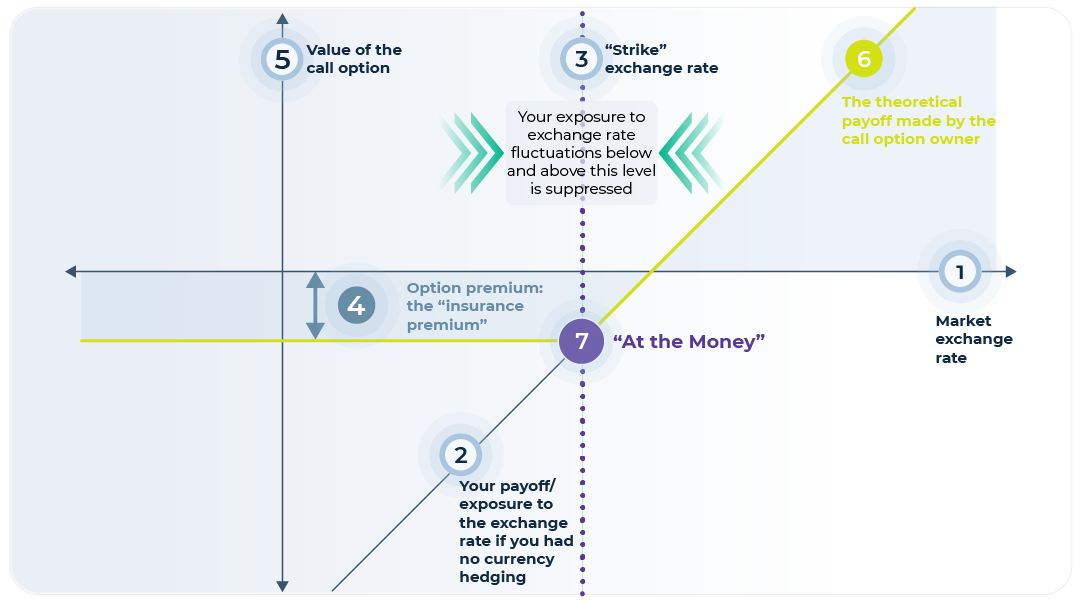

1. Market exchange rate (e.g. USD/GBP) against whose fluctuations you want to protect yourself.

2. Your payoff/exposure to the exchange rate if you had no currency hedging – (i.e. no “insurance”); you can see that it is unlimited both upwards and downwards!

3. “Strike” exchange rate = the exchange rate level that you want to fix for yourself at a specific future date by paying for “insurance” (currency hedging).

4. Option premium: the “insurance premium” – you pay to your currency hedging provider, so that you never lose more money than the premium itself, even if the market exchange rate goes “against” you. This amount is usually equivalent to a small percentage of the foreign-currency income or cost whose value you want to fix (in terms of your home currency), to gain certainty in your business.

5. Value of the call option to its owner (your “insurer”, your currency hedging provider).

6. The theoretical payoff made by the call option owner (i.e. your “insurer”, your currency hedging provider). However, most hedging providers also hedge themselves, to not risk losing too much money, and hence also forfeit all or most of the potential profit. After all, your insurer’s business is not gambling on currency movements, but insuring you properly!

7. “At the Money” – At this point, the market exchange rate is equal to the strike exchange rate. If the market exchange rate is at this level when the call option (your “insurance contract”) expires, then you may ask yourself why you paid an insurance premium. But, remember, had the market exchange rate been below the strike price (“Out of the Money”), you would have been very happy to have this insurance, as it would have limited your total losses to the cost of your insurance premium!

Some Facts

- Options date back to Ancient Greece, when people speculated on olive harvests. But they were popularised in the early 1900s by Jesse Livermore, who speculated on the future prices of stocks he didn’t own.

- There are three main ways to describe value in options trading, or ‘moneyness’. Aside from at the money, an option can also be:

- In the money — this is when the strike price is higher than market value. In the money options are profitable if you’re selling but not if you’re buying.

- Out of the money — here, the option’s strike price is below market value, so it’s profitable if you’re buying but not if you’re selling.

- Options are rarely at the money except at the time they’re written. More often, traders speak of options being ‘near the money’ or ‘close to the money’.

Want to know more?

- This video breaks down the basics of foreign exchange options trading in very simple terms.

- While some of Jesse Livermore’s methods would nowadays be considered illegal, he is still regarded as one of the best traders of all time. This article lists 21 trading lessons taken from his book Reminiscences of a Stock Operator.

ALT21’s perspective:

“SMEs tend to overlook options because they seem too complicated. But they’re an effective way to protect themselves against currency fluctuations. There’s no obligation to make the exchange. So, in the worst case scenario, where the market doesn’t go your way, you’ve only lost a small premium. And in the best case scenario, you’ve locked in a better exchange rate than you’d get on the market.”

At the money vs In the money vs Out of the money

At the money

Strike price = market price

Exercising option usually leads to a small loss (the premium you’ve paid for the option).

In the money

Strike price > market price

Sell at a profit, buy at a loss.

Out of the money

Strike price < market price

Sell at a loss, buy at a profit